OpenSea CEO Fights SEC, Pledges $5 Million to Support Creators Facing Similar Notices

On August 28, Devin Finzer, the co-founder and CEO of OpenSea, revealed that the US Securities and Exchange Commission (SEC) has issued a Wells notice to the NFT marketplace.

This notice, which often precedes legal action, suggests that the SEC believes OpenSea may have violated federal securities laws by facilitating the sale of NFTs that could be considered securities.

Community Voices Clash Over SEC’s Crackdown on OpenSea

Finzer quickly responded, expressing his shock at the SEC’s approach. He argued that NFTs are fundamentally different from securities, describing them as creative goods like art, collectibles, and gaming items.

“We’re shocked the SEC would make such a sweeping move against creators and artists. But we’re ready to stand up and fight,” Finzer asserted.

Furthermore, he argued that the agency’s broad interpretation of securities laws could jeopardize artists’ livelihoods and stifle innovation. Finzer pointed out that NFTs serve various purposes, from gaming items to digital art, and should not be classified as securities under traditional financial regulations. Therefore, to support the broader NFT community, he announced that OpenSea is pledging $5 million to help cover legal fees for NFT creators and developers who receive similar notices.

“Every creator, big or small, should be able to innovate without fear,” Finzer emphasized.

This legal battle has sparked mixed reactions within the NFT community. Some, like Congressman Wiley Nickel, have criticized the SEC’s approach as an overreach that threatens to derail digital innovation in the United States.

“The aggressive use of ‘regulation by enforcement’ from the SEC is a blatant abuse of power that erodes trust and transparency in our regulatory system,” Nickel stated.

Others, like Cameron Winklevoss, co-founder of the crypto exchange Gemini, have echoed this sentiment. He described the SEC’s actions as part of a broader “war on crypto.” Jake Chervinsky, Chief Legal Officer at Variant Fund, also criticized the SEC’s approach.

“The SEC has fully lost the plot. The idea that a financial markets regulator established in the 1930s would have jurisdiction over digital art in the 2020s defies not only common sense but also the SEC’s statutory authority. Thanks to OpenSea for fighting the good fight,” Chervinsky said.

However, not everyone supports OpenSea’s stance. Some figures in the NFT community have expressed relief that the SEC is taking action against what they see as OpenSea’s unethical practices. A prominent figure known as PandaPunk has been particularly vocal, accusing OpenSea of anti-competitive behavior and mishandling user complaints.

Stoner Cats Case Highlights SEC’s Hardline Stance on NFTs

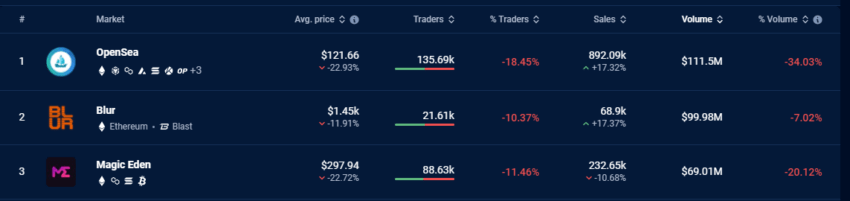

Nonetheless, the SEC’s action against the platform is particularly significant, given OpenSea’s dominant position in the NFT market. DappRadar data shows that, in the past 30 days alone, OpenSea generated over $111 million in sales volume. This figure outpaces its closest competitor, Blur, which recorded $99.98 million.

OpenSea’s NFT Sales Volume Tops Blur and Magic Eden in the Last 30 Days. Source: DappRadar

Indeed, the SEC’s aggressive stance towards OpenSea has amplified the tension in the NFT market. In September 2023, BeInCrypto reported that the SEC took legal action against Stoner Cats (SC2), the entity behind the Stoner Cats animated series.

The charge was for selling NFTs tied to the series without proper registration, essentially offering unregistered securities. Consequently, SC2 complied with a cease-and-desist order and settled the dispute by paying a $1 million fine.

The digital asset industry keenly observes this case’s progress, as its outcome could significantly impact NFTs and the wider digital economy. Ultimately, the resolution hinges on judicial interpretations of the SEC’s actions and their regulatory approach to digital assets.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  Dogecoin

Dogecoin  USDC

USDC  Cardano

Cardano  Hedera

Hedera  Stellar

Stellar  Bitcoin Cash

Bitcoin Cash  LEO Token

LEO Token  Litecoin

Litecoin  OKB

OKB  Algorand

Algorand  Cosmos Hub

Cosmos Hub  Gate

Gate  Maker

Maker  KuCoin

KuCoin  IOTA

IOTA  NEO

NEO  Zcash

Zcash  Polygon

Polygon  Synthetix Network

Synthetix Network  Tether Gold

Tether Gold  TrueUSD

TrueUSD  Holo

Holo  0x Protocol

0x Protocol  Enjin Coin

Enjin Coin  Basic Attention

Basic Attention  Siacoin

Siacoin  Ravencoin

Ravencoin  Decred

Decred  Ontology

Ontology  DigiByte

DigiByte  Nano

Nano  Status

Status  Waves

Waves  Steem

Steem  Numeraire

Numeraire  Pax Dollar

Pax Dollar  BUSD

BUSD  OMG Network

OMG Network  Ren

Ren  Bitcoin Diamond

Bitcoin Diamond