Why You Should (Still) Care About Silvergate

Last week, I published a new article revisiting the last days of the doomed pro-crypto bank Silvergate, alleging that it had been effectively killed off by federal regulators within the Biden administration. You may be wondering why I am relitigating events that took place in the spring of 2023.

The truth is, I believe that those fateful events are widely misunderstood, and that hindsight has brought us more information to better understand what really took place. The conventional narrative is that Silvergate, Signature, and others were the architects of their own demise. They accepted crypto firms as clients and paid the price when the crypto space experienced tremors in 2022 and 2023; and mismanaged the maturity of their asset portfolio throughout a period of rising rates.

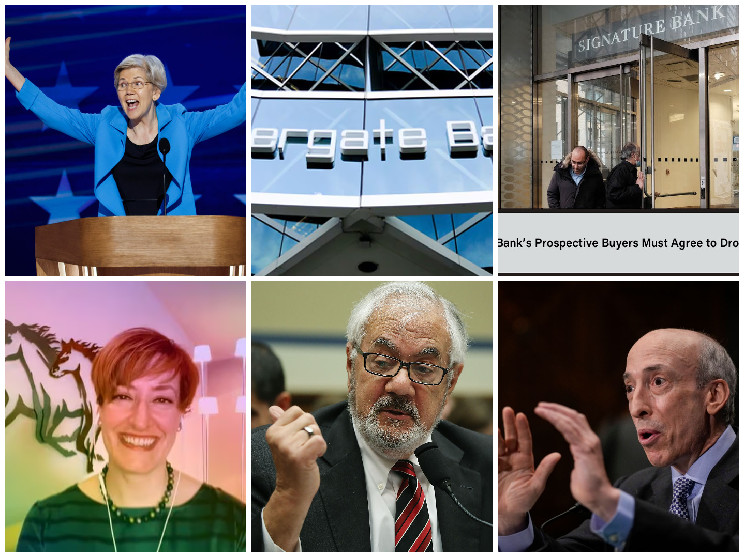

But I hold a different view. In my opinion, we have evidence enough to suggest that the two most important pro-crypto banks, Silvergate and Signature, were opportunistically executed amid the fog of war during the 2023 banking crisis, as part of a broader coordinated attempt to de-bank the crypto industry. The Biden administration went far further than simply discouraging banks from serving crypto; they actually shuttered the two most critical banks that were serving the sector. This brazen scheme has never been talked about in DC. Establishment post mortems of the banking crisis focus on interest rates, maturity mismatches in asset portfolios and depository flight.

We have enough evidence now to make sense of what really happened. One sign that something was amiss was Signature board member Barney Frank alleging that the bank was shut down “because of our prominent identification with crypto.” A banker familiar with the process told me: “Signature wasn’t even given a chance to raise capital and save themselves. It was definitely an execution.” For their part, the New York Department of Financial Services, the state’s main regulator, denies this.

There were also significant irregularities in the process of selling Signature. FDIC refused to allow Flagstar, Signature’s acquirer, to take ownership of $4 billion of deposits from crypto firms. The funds were forcibly sent back to depositors. The sale of Signature’s SigNet network, which allowed bank crypto clients to transact between each other 24/7, was also stymied. One banker involved in the process told me that Tassat (the developer of SigNet tech) was interested in buying back the asset.

Apollo Global Management had also lined up a consortium to place a bid. The person familiar with the situation told me: “The FDIC didn’t put it in writing, but they called during the bidding process and told us verbally ‘Don’t bid on the crypto products.’” The auction for SigNet finally went live on Friday, June 9 2023 – the week that the SEC sued Binance and Coinbase. There were no bids and the SigNet asset was furloughed completely.

As a reminder, the FDIC’s stated mandate is to maximize taxpayer value by arranging the sale of all bank assets, not just the ones that are politically benign. A subsequent memo from the Congressional Research Service noted that “This reluctance [of banks to serve crypto] was evinced by the FDIC’s announcement that it will return Signature’s deposits to crypto firms…,” acknowledging that the FDIC’s excising of Signature’s crypto business was a telling. The WSJ Editorial Board, for its part, felt that this was a smoking gun, writing “This [refusal by the FDIC to sell the crypto business] confirms Mr. Frank’s suspicions — and ours — that Signature’s seizure was motivated by regulators’ hostility toward crypto.”

And then there’s Silvergate. Silvergate was never sold, but rather voluntarily liquidated by management. None of its executives have since dared speak up. In early 2023, the SF Fed communicated to them, with the seeming tacit approval of other regulators, that they would have to reduce their crypto deposits to a de minimis share of their overall business. This was fatal to its practice – as over 90% of their deposits related to the crypto space as of Q2 2022. Following the bank run in Dec. 2022-Jan. 2023, Silvergate was still solvent. After all was said and done, they were able to make all depositors whole, even though they were cut off from last-resort liquidity at the FHLB thanks to a pressure campaign from Sen. Elizabeth Warren (D-MA).

Perversely, Silvergate leadership have not been able to speak up regarding the sudden change in regulatory policy, as they have been busy settling cases with their regulatory overseers, alongside class actions. Revelations regarding the informal cap on deposits that made their business impossible are considered “confidential supervisory information” and hence ineligible to be publicly shared.

However, in recent bankruptcy filings, Silvergate Chief Accounting Officer Elaine Hetrick for the first time laid out Silvergate’s version of the story. She directly accuses regulators of forcing a shutdown of the bank, writing: “This public signaling and sudden regulatory shift made clear that, at least as of the first quarter of 2023, the Federal Bank Regulatory Agencies would not tolerate banks with significant concentrations of digital asset customers, ultimately preventing Silvergate Bank from continuing its digital asset focused business model.”

Both Silvergate and Signature faced rumors during the panic of 2023 that they were under criminal investigation relating to their dealings with the crypto space. Silvergate was infamously a service provider to FTX. These allegations formed a large part of the case against the banks made by high profile short sellers – as well as Warren. No criminal allegations ever materialized. Silvergate settled with regulators for surveillance outages on SEN, the bank’s exchange network. It settled with the SEC with respect to perceived inaccuracies in statements made by management regarding their compliance program.

Thus, the passage of time has brought things into focus. The allegations of criminality swirling around the banks ended up being vacuous. New filings from Silvergate lend credence to the idea that they were liquidated by political mandate. And, since the crisis, bank regulators have continued to harass banks known to serve crypto, like Customers and Cross River, who have both been hit with enforcement actions or consent orders.

Newer banks are being prohibited from filling the gap, too. Custodia continues to wage a protracted legal campaign to obtain a master account at the Fed, a necessary precondition to becoming a full-fledged bank. Meanwhile, Protego Trust Company, which had received a preliminary federal charter from the OCC, saw its charter revoked. Not only were existing pro-crypto banks killed off, and new aspirants discouraged from doing business with the sector, but newer entrants were simply prohibited from opening their doors. Within the conventional banking sector, bad rules like the SEC’s SAB121 (whose congressional overturn was vetoed by Biden) effectively prohibit banks from touching crypto. The Fed has also issued dire warnings about banks wanting to do business with stablecoins. The crackdown on crypto via financial regulation has been incredibly comprehensive and involved every important U.S. financial regulator.

U.S.-based crypto entrepreneurs and operators know first-hand that obtaining banking is uniquely challenging – harder than it should be. Even though we in the crypto space are the primary victims of this round of financial repression, this issue goes far beyond crypto. Ultimately, it’s about the government unconstitutionally choosing to marginalize a specific (legal) industry, not by passing a law or with notice-and-comment rulemaking, but via covert, informal threats made to bankers.

As the law firm Cooper & Kirk has argued, this kind of financial redlining is a violation of the due process clause in the Fifth Amendment, because affected firms are not given the opportunity to challenge these rules. Secret, informal rulemaking also may violate the administrative procedures act. Ultimately, this issue comes down to the fundamental question: should banking infrastructure – effectively an arm of the state – be weaponized for political ends, or should it remain neutral, free for any legal business to rely on?

Sadly, the contemporary left appears comfortable using bank regulation against political disfavored industries, both under Obama and again under Biden. While Trump was more reticent to employ the same tactics, it’s not inconceivable that the shoe could be on the other foot soon. There is a partisan tinge to the fact-pattern but there doesn’t have to be one. As a highly regulated industry with barriers to entry, banking should not be deputized for arbitrary political ends. Crypto is the latest victim of this misbehavior, but this issue should deeply concern anyone.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc. or its owners and affiliates.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  USDC

USDC  Dogecoin

Dogecoin  Cardano

Cardano  Bitcoin Cash

Bitcoin Cash  LEO Token

LEO Token  Litecoin

Litecoin  Stellar

Stellar  OKB

OKB  Hedera

Hedera  Cosmos Hub

Cosmos Hub  Maker

Maker  KuCoin

KuCoin  Gate

Gate  Algorand

Algorand  Polygon

Polygon  NEO

NEO  Zcash

Zcash  Tether Gold

Tether Gold  Synthetix Network

Synthetix Network  TrueUSD

TrueUSD  IOTA

IOTA  Holo

Holo  0x Protocol

0x Protocol  Siacoin

Siacoin  Enjin Coin

Enjin Coin  Ravencoin

Ravencoin  Basic Attention

Basic Attention  Decred

Decred  Ontology

Ontology  Numeraire

Numeraire  Nano

Nano  Pax Dollar

Pax Dollar  DigiByte

DigiByte  Waves

Waves  Status

Status  Steem

Steem  BUSD

BUSD  Ren

Ren  OMG Network

OMG Network  Bitcoin Diamond

Bitcoin Diamond  Bytom

Bytom  HUSD

HUSD