A Deep Dive into Bitcoin Mining Veteran Hut 8

A deep dive into Hut 8 Mining, uncovering its often overlooked business sectors. Understand its financial performance, strategic initiatives and HPC/AI developments.

The following guest post comes from Bitcoinminingstock.io, providing comprehensive data, in-depth research, and analyses on Bitcoin mining stocks. Originally published on Nov. 29, 2024, it was penned by Bitcoinminingstock.io author Cindy Feng.

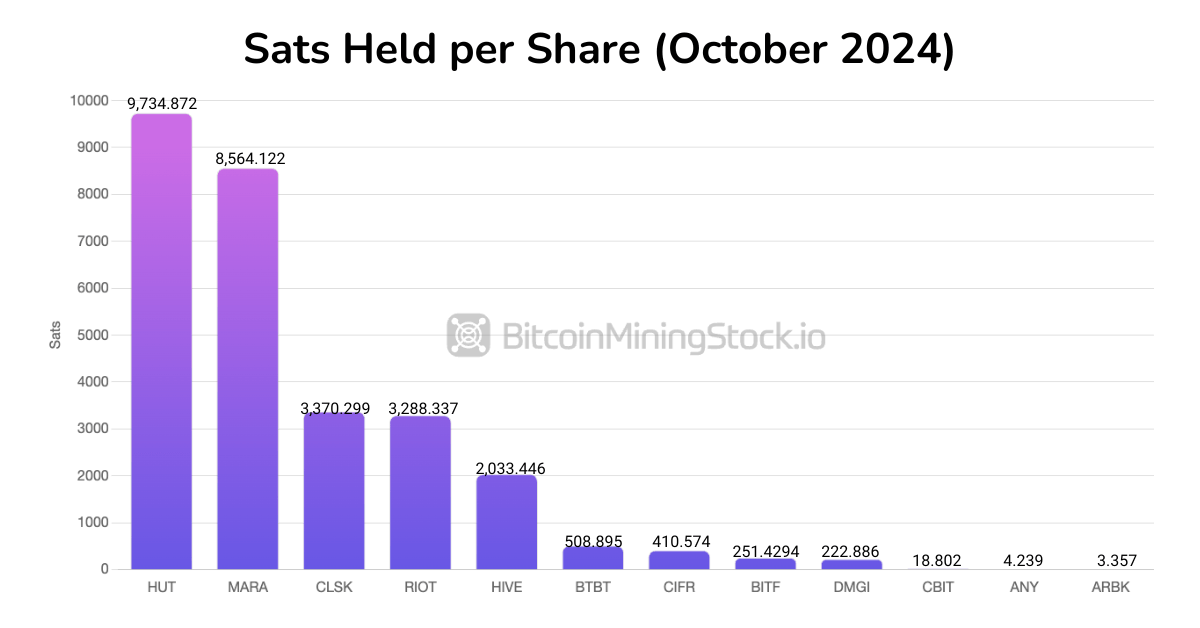

The YTD performance of Hut 8 Mining Corp. (NASDAQ: HUT) has made it a standout. Other metrics like Satoshi per share are also eye-catching, where Hut 8 outperforms MARA and where the latter is the largest Bitcoin holder among all public Bitcoin mining companies. As one of the first Bitcoin miners to go public (initially listed on the TSX in 2018 and later on Nasdaq in 2021) Hut 8 has experienced the full spectrum of market cycles. By analyzing this Bitcoin mining veteran, we can gain valuable insights to better navigate the ever evolving industry.

Source: https://bitcoinminingstock.io/holdings

Basic Profile

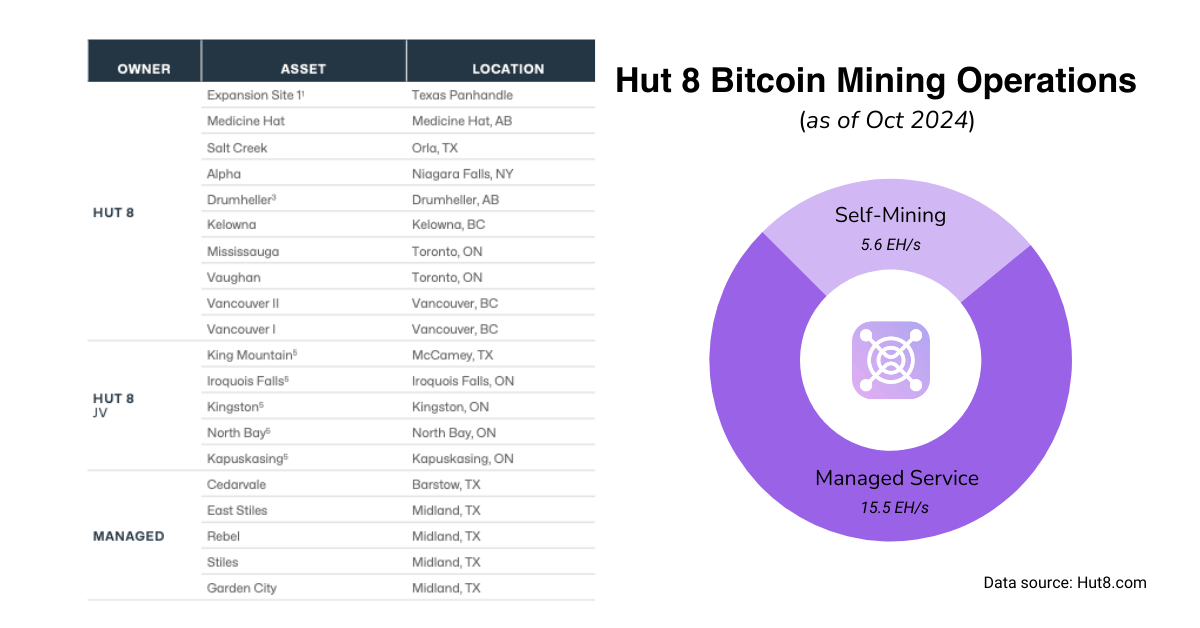

Hut 8 is a Bitcoin miner with operations in Canada and the United States. The company currently has 20 sites in its portfolio, comprising both operational facilities and others currently under development. At the time of writing, Hut 8 reported a combined capacity of 967 MW, equivalent to 20.1 EH/s. This includes 5.6 EH/s for self-mining, and the rest allocated to managed services.

Beyond its core mining operations, Hut 8 engages in Bitcoin mining equipment sales and repairs. Additionally, the company’s Far North JV site participates in grid balancing programs through natural gas power plants in Ontario, Canada.

In July, Hut 8 announced the closing of a $150M investment from Coatue, and then launched GPU-as-a-Service in September. It’s clear that the company is accelerating its position in the HPC/AI sector. In recent marketing materials, Hut 8 describes itself as an “energy infrastructure platform”, which also signals a gradual move away from Bitcoin mining as its sole focus.

Q3 Performance

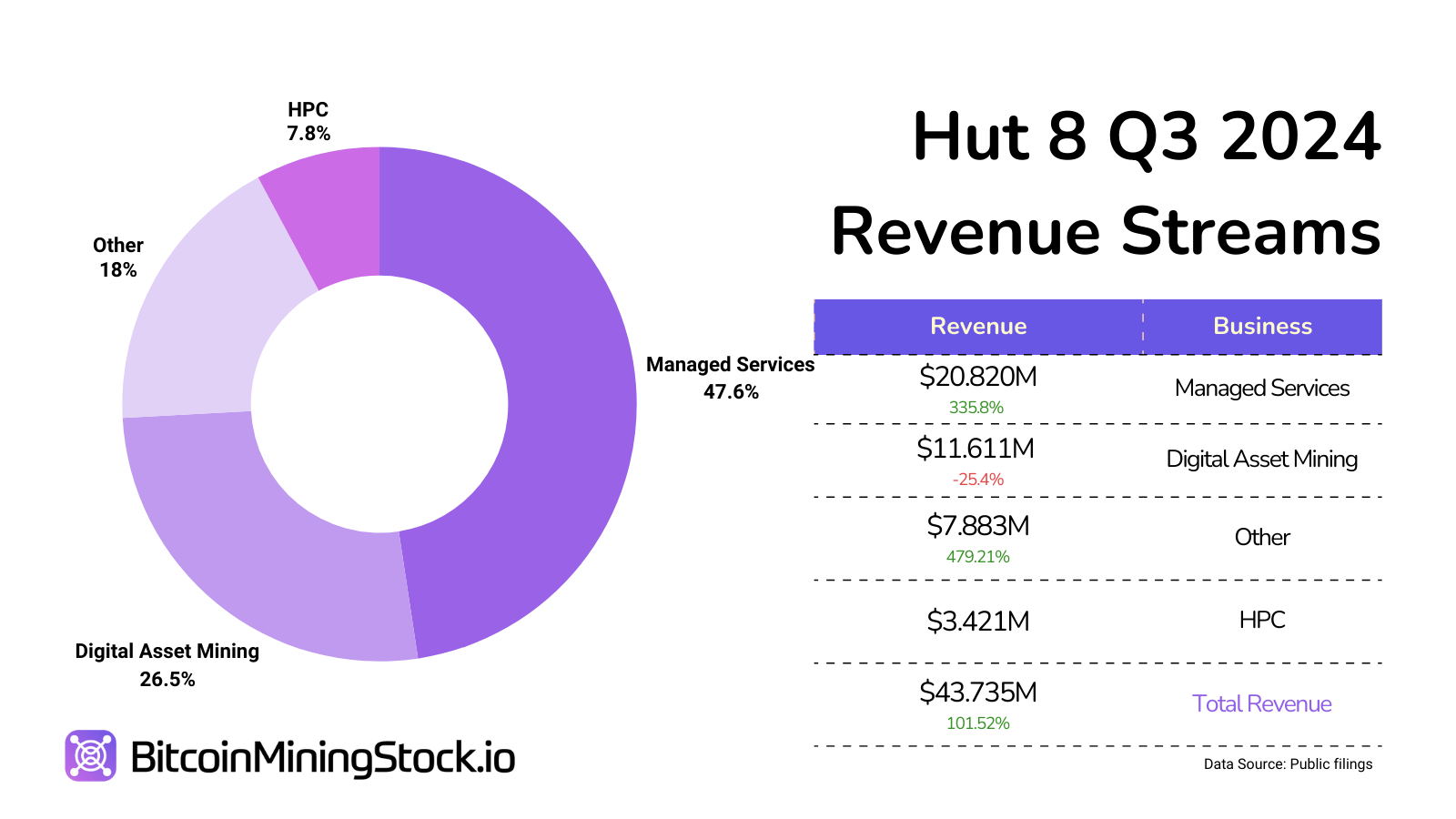

In Q3 2024, Hut 8 demonstrated robust revenue growth and strategic execution driven by diversification into HPC and energy-efficient mining.

Total revenue for Q3 2024 rose significantly to $43.7M, a 101% increase compared to the same period last year (24% QoQ increase). This growth was fuelled by managed services revenue, which surged 336% to $20.8M, and HPC services contributing $3.4M. Digital asset mining revenue however fell by 25% to $11.6M, reflecting the impact of increased Bitcoin network difficulty and the April 2024 halving event.

Net income turned positive at $0.9M compared to a $4.4M loss in Q3 2023. However adjusted EBITDA fell to $5.6M, a 51% decrease, driven largely by a sharp rise in operating expenses. Notably, stock-based compensation alone accounted for $4.96M, a 1536% YoY increase.

On the operational front, Hut 8’s efficiency efforts resulted in a 33% YoY reduction in energy costs to $0.029 per kWh. However Bitcoin mining costs increased to $31,482 per BTC when considering energy costs alone, indicating areas that require further optimization to maintain profitability.

Managed Services: Stable Recurring Revenue

Managed services, though often overlooked by analysts, accounted for nearly half of Hut 8’s total revenue in Q3 and exhibited the largest YoY growth among all business segments. These services involve comprehensive project management for customers’ data centers including design, construction, and ongoing operation, tailored to the clients’ specific needs. Governed by long-term Project Management Agreements (PMAs) that typically span four to ten years with potential renewal options, these services provide a stable revenue stream.

The revenue from managed services is derived from a mix of fixed monthly fees, variable reimbursements, and occasionally equity-based compensation. In Q3, management fees increased to $4.1M from $3.4M in the same period last year, while cost reimbursements rose to $1.9M from $1.4M. Additionally, the company received $1.3M in customer equity and a one-time termination fee of $13.5M from MARA related to the termination of PMAs for the Kearney and Granbury sites.

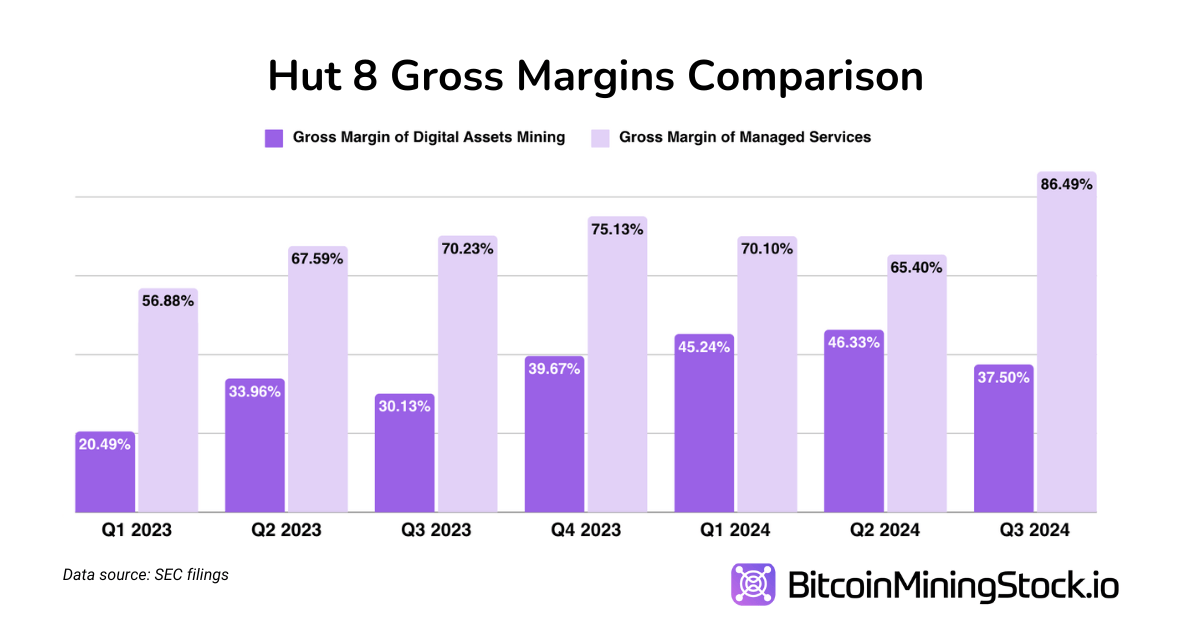

Excluding one-off revenues, the recurring income from managed servicesstands at approximately $6M per quarter. Not to mention its around 70% of the gross margin rate. This may explain why Hut 8 allocates nearly half of its total hashrate to managed services. It also validates Hut 8’s expertise in data center operations and makes the new brand as an “energy infrastructure platform” more convincing.

For Hut 8, the gross margins of managed services are higher than those of Bitcoin mining, and this remains consistent even after the Bitcoin Halving.

AI and HPC Ventures: Diversification with Strategic Backing

Hut 8’s HPC/AI revenue only increased by 1.66% compared to last quarter, but the growth potential of this segment appears promising. In July the company secured a $150M investment from Coatue Management, a renowned technology-focused investment firm with over $47B in assets under management. Coatue is known for its strategic investments in GPU infrastructure and AI data centers, having backed high-profile companies such as Tesla, ByteDance, and Stripe.

Hut 8 Joins Coatue’s AI Portfolio (screenshot from its presentation deck)

This partnership provides Hut 8 with critical capital for deploying and scaling AI and HPC infrastructure, including NVIDIA H100 GPUs in its GPU-as-a-Service vertical. Moreover, it grants access to Coatue’s network of technological expertise and market insights, enhancing Hut 8’s credibility and market position in the AI and HPC sectors.

The success of this venture depends on Hut 8’s ability to capture market share in a competitive landscape dominated by established HPC providers. Regardless, Coatue’s backing signals confidence in Hut 8’s strategy, infrastructure, and execution capability.

P.S. Hut 8’s HPC services primarily include colocation and cloud solutions. To understand technical aspects, you may find this article from Digital Mining Solution helpful.

Strategic Initiatives: ASIC Fleet Upgrade and BITMAIN Partnership

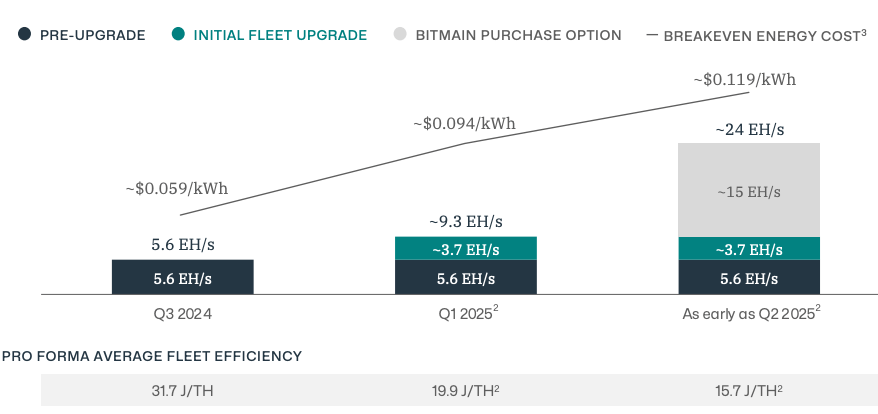

Hut 8 has undertaken significant strategic initiatives to enhance its mining capabilities and operational efficiency. In early November, the company announced an ASIC fleet upgrade with the initial purchase of 31,145 BITMAIN Antminer S21+ miners, scheduled for deployment in early 2025. This upgrade is expected to boost Hut 8’s self-mining hashrate by approximately 3.7 EH/s to a total of 9.3 EH/s, representing a 66% increase. This will improve energy efficiency by reducing consumption by 37%, achieving an efficiency rate of 19.9 J/TH.

Hut 8 Fleet Upgrade Summary (screenshot from its Q3 Results Deck)

Earlier in September, Hut 8 entered into a 15 EH/s colocation agreement with BITMAIN at their Vega site, expecting the deployment of next-generation U3S21EXPH miners in Q2 2025. To fully leverage liquid-to-chip cooling technology, Hut 8 has developed a custom design for its Bitcoin mining data center infrastructure. Their agreement includes a purchase option, enabling Hut 8 to potentially scale its self-mining hashrate to around 24 EH/s by mid-2025.

Capital Structure and Liquidity

As of Q3 2024, Hut 8 had $72.3M in cash and digital asset holdings valued at $576.5M. The company’s conversion of a $37.9M loan with Anchorage Digitalinto equity improved its balance sheet by eliminating future interest obligations of approximately $17M over three years.

Despite this, Hut 8’s stock-based compensation rose significantly in 2024 (for the nine months ending September 30) after reaching $16.4M—an 895.8% YoY increase compared to the same period last year. Additionally, the company’s reliance on Bitcoin sales for liquidity ties its operational funding to market conditions, exposing it to potential cash flow volatility during bearish cycles.

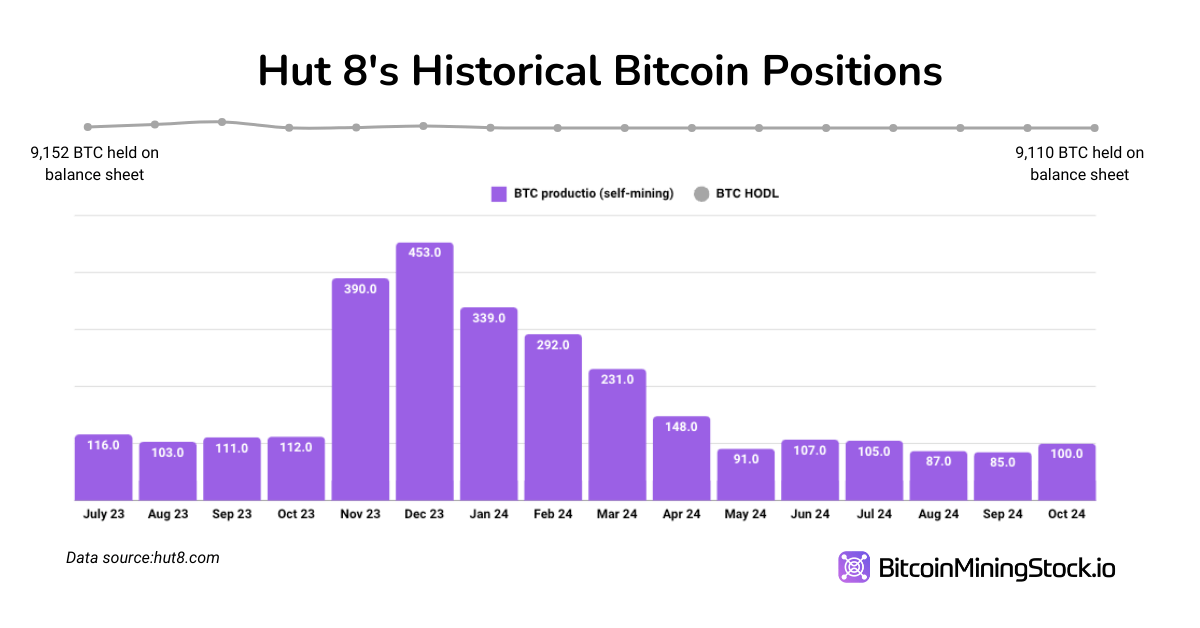

The public record of Hut 8’s Bitcoin treasury can be traced back to August 2021. Throughout 2023 and until October 2024, Hut 8’s BTC holdings remained around 9,100 BTC, indicating that the company has been periodically selling newly minted Bitcoin.

Final Thoughts

Earlier this year, investigative research company J Capital Research questioned Hut 8’s acquisition of USBTC and the qualifications of its leadership. Despite these criticisms, Hut 8 has delivered measurable improvements: from energy efficiency, strategic partnerships to disciplined capital management and investors can observe tangible changes. This veteran Bitcoin mining company now pivots toward becoming an energy infrastructure platform with a focus beyond mining. With Coatue’s investment, its AI and HPC services are positioned for growth in the coming quarters. Personally, I feel Hut 8 remains a compelling opportunity because its past and present perfectly demonstrate how to adapt and thrive in an ever-evolving industry.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  Dogecoin

Dogecoin  USDC

USDC  Cardano

Cardano  Stellar

Stellar  Hedera

Hedera  Bitcoin Cash

Bitcoin Cash  LEO Token

LEO Token  Litecoin

Litecoin  Algorand

Algorand  OKB

OKB  Cosmos Hub

Cosmos Hub  Gate

Gate  Maker

Maker  KuCoin

KuCoin  IOTA

IOTA  NEO

NEO  Polygon

Polygon  Zcash

Zcash  Synthetix Network

Synthetix Network  Tether Gold

Tether Gold  TrueUSD

TrueUSD  Holo

Holo  Enjin Coin

Enjin Coin  0x Protocol

0x Protocol  Basic Attention

Basic Attention  Siacoin

Siacoin  Ravencoin

Ravencoin  Decred

Decred  Ontology

Ontology  DigiByte

DigiByte  Status

Status  Nano

Nano  Waves

Waves  Numeraire

Numeraire  Steem

Steem  Pax Dollar

Pax Dollar  BUSD

BUSD  OMG Network

OMG Network  Ren

Ren  Bitcoin Diamond

Bitcoin Diamond  Bytom

Bytom